Under changes announced by Government during the last budget, KiwiSaver contribution rates are due to increase by half of a percent on April 1st.

Currently the minimum employee contribution rate is 3% and the same goes for employers. It will automatically nudge up to 3.5% for both you and your employer. The move is aimed at increasing private savings and moving New Zealander closer into alignment with national savings rates in other countries.

Most employees won’t notice it much, not at least in the short-term. But for those struggling to make their daily expenses currently, it could feel a little a painful.

For that reason, employees who feel they can’t manage the extra will be able to apply for a temporary rate reduction.

Given the long-term advantage of contributing that 1% extra, it makes good sense for most people to go with the flow.

Remember, savings rates in Australia are closer to 12%. We are still a long way behind in New Zealand.

Those who can’t manage, and apply for the exemption, will be able to hold their contribution rates at 3% for a year only. After that, it’ll move to 3.5% unless you do something more radical i.e. apply for a savings suspension whereby you stop contributing altogether for a period of up to five years.

You won’t find many financial educators, fund managers or advisors advocating you hold your contribution rate at 3% or else pause it altogether. The benefit of higher contribution rates is very clear over time in terms of how much extra you’ll have saved up when it comes time for that first home deposit or retirement.

Visit the IRD’s KiwiSaver note on changes here.

One percent may not seem like much but over time, with the magic of compounding interest in the context of an investment vehicle, it adds up.

On a base salary of $65,000, over 20 years, assuming an average rate of return of 4.5%, it’s roughly $20k extra. For the

| Contribution Rate | Annual Total | 20-yr Balance |

|---|---|---|

| 3% + 3% | $3,900 | ~$122,350 |

| 3.5% + 3.5% | $4,550 | ~$142,740 |

| Difference | +$650 p.a. | +$20,400 |

The plan for incremental increases doesn’t stop at 3.5% in April.

Another bump is planned for April 2028, bringing employee and employer contribution rates up to 8%. It is worth noting, that you can optionally contribute 4%, 6%, 8% or 10% currently. (Some employers do contribute at a higher rate than the minimum 3%).

Worldwide, the targeted savings rate for retirement was around 10% of gross income, 15 years ago. So the move to get New Zealand savers more is hardly an over reaction. We’re well behind as a nation.

What’s your Number? See my previous blog on contribution rate comparisons here.

One size does not fit all when it comes to retirement savings of course.

Some people will need more, some less, and others will have savings and income strategies for retirement outside of KiwiSaver that will help them manage.

The important thing is to know where you’re at presently, and where you’d like to be in the future. Then it’s a matter of making adjustments. Those adjustments can include earning more, spending less, downsizing your home, or arranging your life differently.

Living in metropolitan areas is generally more expensive than living in the provinces. Some will be planning their future with spouses or family members. That can also change the outlook as will moving to cheaper countries like Thailand or Bali in retirement.

It’s easy to become overwhelmed, stick your head in the sand and do nothing. Please don’t.

What can you do today?

Grab your latest pay stub and log into your KiwiSaver provider’s website and find out what you’re currently contributing, what your fund type is, and read your last annual member statement which shows you what you’re on track to have at 65.

If the number is not what you know you’ll need to live on, don’t panic!

Use Sorted.org.nz’s KiwiSaver calculator to find out what different contribution rates can make overtime and think about how you can rearrange your life to get to your desired goal.

Just about the worst thing you can do is to ignore the fact that one day you will need those savings in the absence of another funding source.

This is where one percent will reduce the freak out factor. On a salary of $65k, it amount to an extra $27 a month in contributions. In practical terms, it’s the equivalent of an extra flat white a week but it makes you richer rather than poorer and plumper.

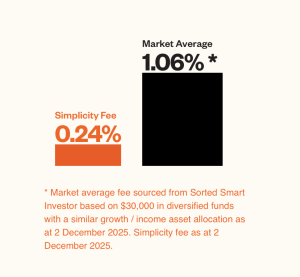

It’s also worth noting that when it comes to the fees you pay on KiwiSaver, a one percent difference over time is also impactful.

To find out just how much, use Simplicity KiwiSaver fees comparison calculator here which shows you how much most KiwiSaver providers charge, versus a low-cost nonprofit index fund.

There’s a good reason this Kiwi start up has grown to more than $10 billion in funds under management in less than 10 years. Members tend to understand the effect of compound interest.

Note: The information above should not be construed as personalised financial advice and is for informational purposes only. While a co-founder of Simplicity I do not receive any remuneration or benefit from promoting the company or its fund. I am a volunteer.