I’m sure a few Millenials choked on their oat milk lattes this week when they read the latest news about how much they’ll need to have saved to enjoy a comfortable retirement.

According to researchers at NZ’s Massey University’s Fin-Ed Centre, if you want to have a retirement that comes with ‘choices,’ you’ll need around $755k in your KiwiSaver or an equivalent savings vehicle.

Oh, and that figure also assumes you have paid your mortgage in full, or you’re living rent-free then retirement.

Given the average amount saved by New Zealanders currently is around $30k, many will be working well past retirement age to afford those flights to Bali or to visit their future grandkids in Australia.

Of course, where you’re at savings-wise depends on a range of factors, not the least of which is how long it is before you actually stop working for a living.

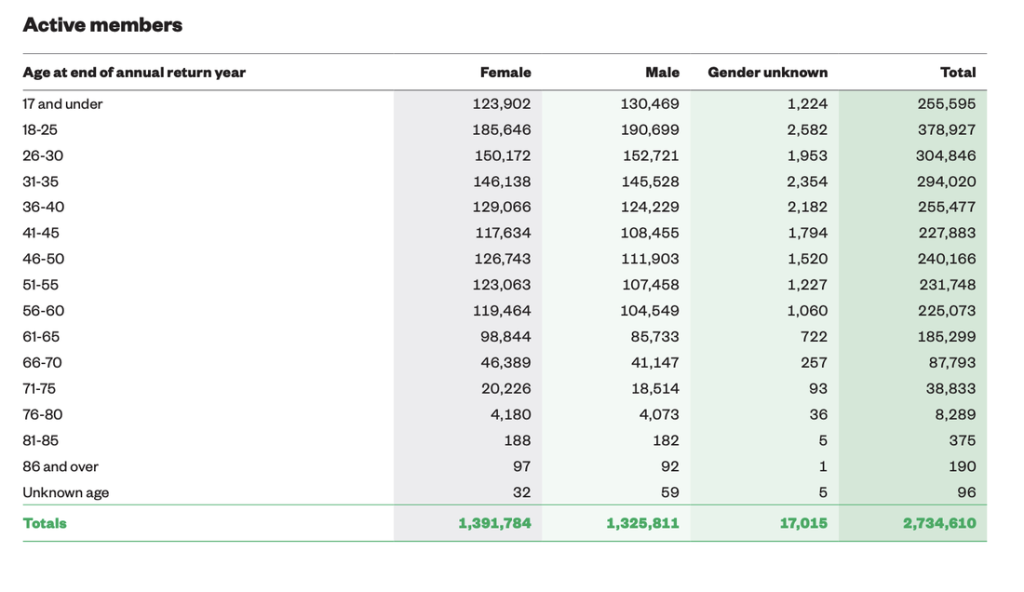

The Financial Markets Authority, which serves up an annual report on KiwiSaver full of juicy stats, provides a nifty breakdown of how many investors are by gender (yes, so passe) and age.

You can see the bulk of them have a long way to go to reach the golden age of 65, and thereof

have plenty of time to pad that nest egg, that will hopefully buy them choices in their golden years.

Most people should be concerned about their current levels of savings, but the reality is most will not have read this latest research or even have a clue who their KiwiSaver provider is, let alone know their balance.

The truth is, numbers scare people. And true to the reptilian brain which we have yet to evolve from, they will run rather than face their fears and take action to deal with a savings shortfall that is potentially avoidable.

The sad reality is that it doesn’t take much effort to figure out the above and set a course of action.

So for those who don’t know, or even know but want to help someone who doesn’t, here’s a simple plan:

- If you don’t know who your provider is, find out today. If you have an IR login, it will be stated on your records there. If you don’t have online access, for Pete’s sake register. You can do all sorts of financially helpful things there, including recording bank payment information. Bonus: If you’re eligible, you’ll get the following cost of living payment from the Gov’t. Thousands didn’t because IR didn’t know how to pay them. If you can’t figure this out, it’s time to go old school and pick up the phone. 0800 257 777

- Once you have your provider’s name, create your online access to your KiwiSaver account. You should be able to do this via their website or by calling their customer service line. Check your balance, your fund type and your PIR. The default rate for PIR is 28%, so you may be overpaying or underpaying, but there are now systems in place by the IRD to pick up the latter.

- Look at your last annual statement to find out how much you’re on track to have at your current savings rate. Most of these are filed within the member area of your account, but if you can’t find the most recent one, pick up the phone and ask your provider to send you a copy by email or snail mail.

Your annual KiwiSaver report shows you how much you’re on track to have by age 65 based on your current contribution rates and fund type. This is a conservative estimate, as the FMA introduced a standardised calculation method a few year ago using conservative long-term figures. They did this because some providers rather sneakily for the purposes of luring new customers used sky-high annual figures based on bull market double-digit returns, annualised over 40 years. In other words, they overstated what you’re actually likely to earn over the working life of KiwiSaver when factoring in market cycles and meltdowns, like what we’ve currently seen. For these long-term projections, they are based on returns of:

4.5% for a Growth Fund

3.5% for a Balanced Fund

2.5% for a Conservative Fund

You can also read some of the FMA’s scenarios on their website based on differing income and contribution levels which will give you an idea of how a 3% contribution rate looks long-term to 4% or higher. They also discuss boring but important things like inflation (which, as we now know, matters) as well as the inclusion of superannuation contributions. Also, handy. Pray that’s still on offer when you retire.

Okay, so now that you know how much you might expect in retirement, you have a few options for addressing any potential shortfall. Please note: this is not personalised advice, only information for you to consider:

- Increasing your contribution rate IF that makes sense for you personally. The minimum is 3% for you and your employer, but YOU can also increase your share to 4, 6, 8 or even 10%. Whether that makes sense for you will depend on your personal circumstances. I.e. are you carrying high-interest credit card debt at 18% that you are ignoring but which you would be smart to pay off?!

- Changing your fund type to one that is likely to produce a higher rate of return over time IF you can sleep with volatility, aren’t looking to withdraw your funds for a first home deposit any time soon, and aren’t within firing range of retirement age.

- Consider options to increase your earning ability, i.e. second jobs, a change of career, working longer etc.

- Spending less. This is the obvious and seemingly most straightforward option, but most people lack the discipline to spend less because they’ve been trained to become faithful consumers of stuff they don’t need. These are challenging times, and life is expensive, so cutting spending may be more difficult these days, especially when inflation is 7% and everything costs more. I’m not saying it’ll be easy but if we’re honest with ourselves, a lot of spending is nonessential. And yes that includes nail colour and gym membership that don’t get used.

Whatever path you choose is your choice, and comes down to priorities and goals. Whatever you do, don’t use lack of information as an excuse. Everything is out there ready for you to discover. And thanks to more rigorous regulatory enforcement in recent years, the financial services sector can no longer be blamed for making information hard to find or understand. Time to stop looking for scapegoat’s and take action.